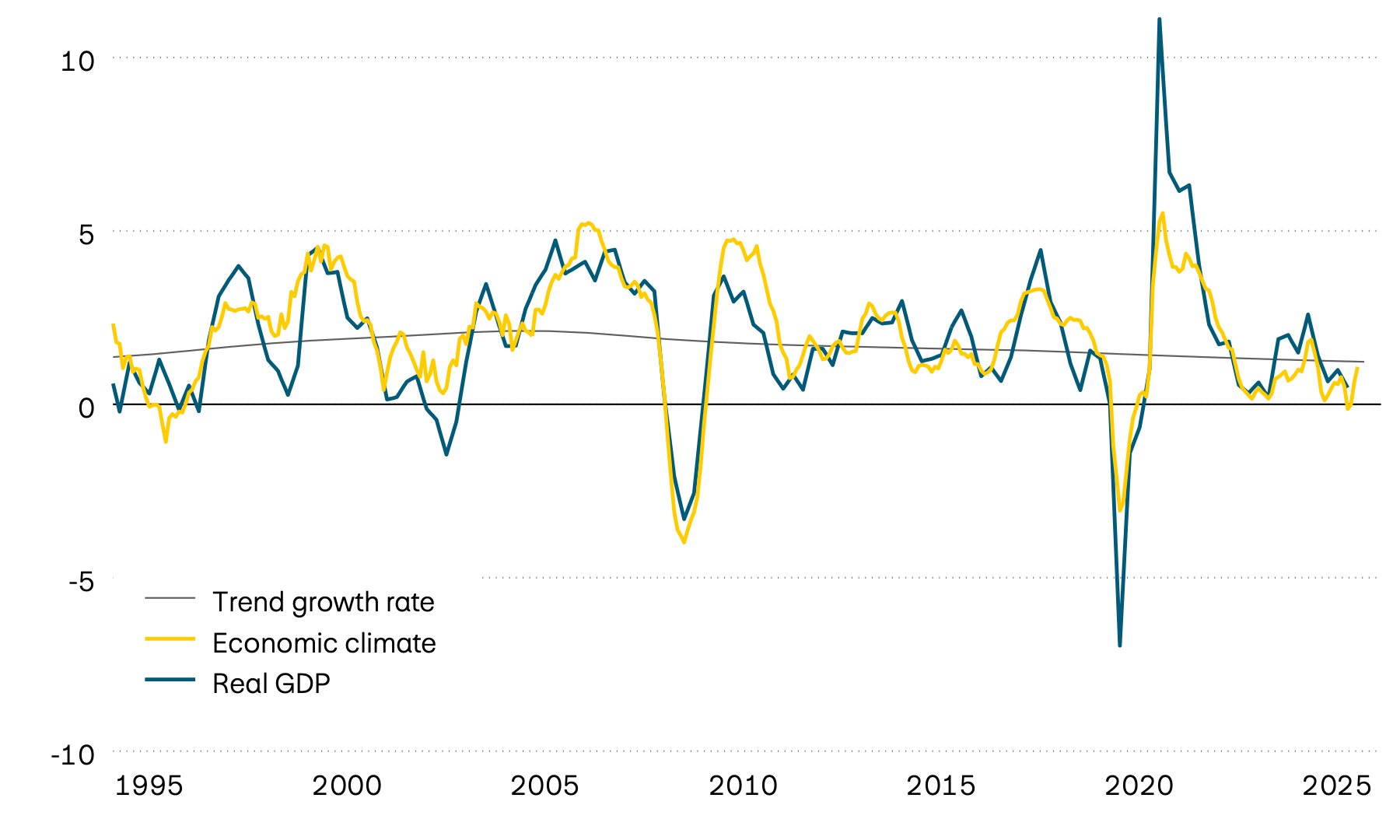

After a challenging 2025, the Swiss economy gradually appears to be regaining its footing. It gathered some momentum again in the first few months of 2026, which is also reflected in sentiment among industrial and service companies, which are expecting business activity to increase again. Consumer activity also picked up again to some extent recently, although the Swiss public remains cautious overall in view of geopolitical tensions and the difficult economic environment. The fact that inflation in Switzerland is exceptionally low by international standards is also likely to be helpful for consumer activity: despite higher energy prices, inflation currently stands at just 0.5 percent. This gives the Swiss National Bank (SNB) the leeway to continue providing support through its monetary policy.

Economy: Swiss economy picks up speed

After a difficult year in 2025, the Swiss economy has recovered slightly recently. Together with Japan, it’s one of the few economies to post a clear upward trend. In the USA, the picture is increasingly mixed; in the eurozone, the economic weakness is continuing for the time being, and China remains in crisis. As such, the global economic environment remains challenging, especially as inflation remains too high in many economies.

Growth, sentiment and trend

In percent

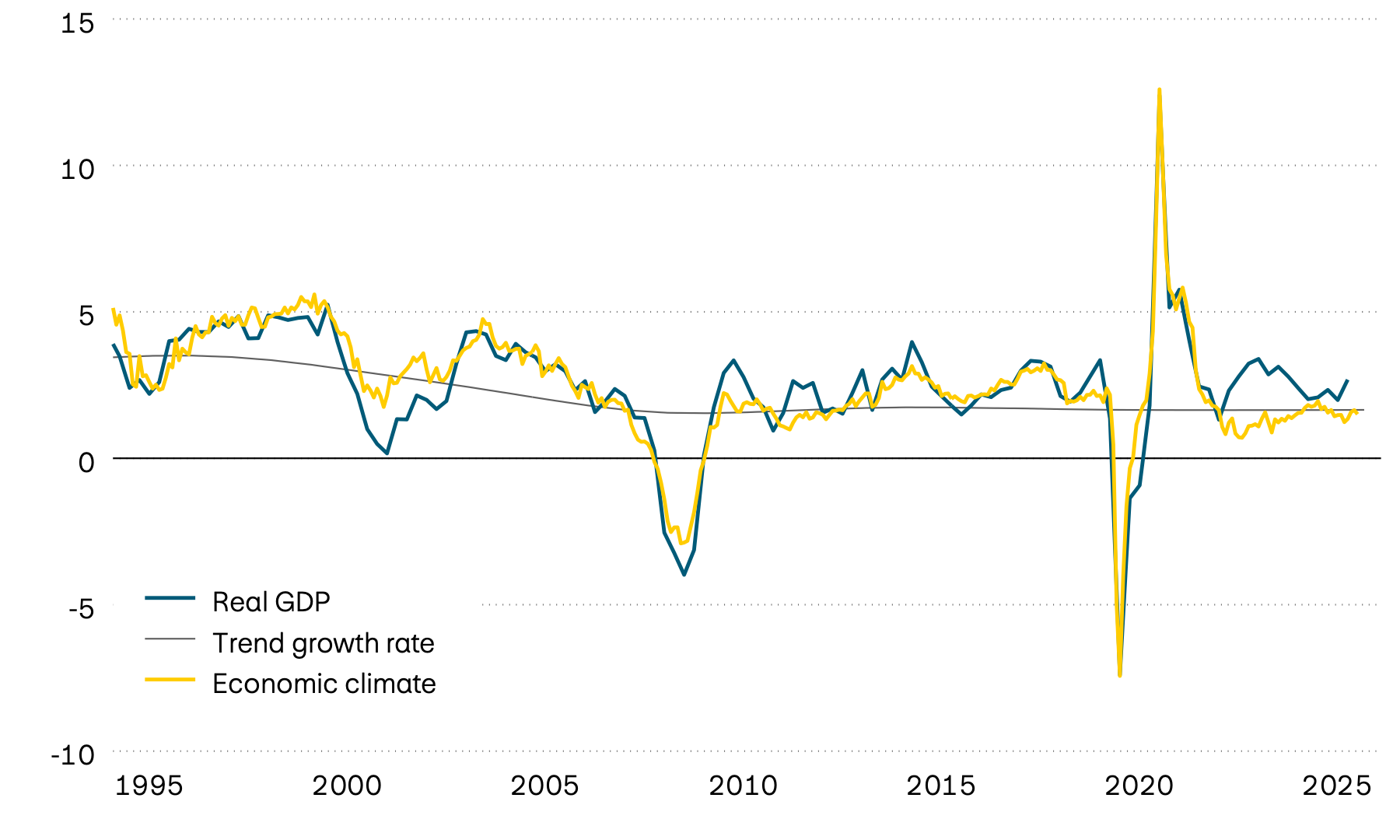

The economic picture in the largest economy remains uneven. US companies remain optimistic, which supports investment activity and helps to stabilize the labour market. Since the start of the year, more jobs have been created, following a decline in employment towards the end of last year. Consumers, on the other hand, remain extremely pessimistic, which is hardly surprising given the rise in inflation that has clearly exceeded income growth since the start of the year. The weakness in the construction sector has also become more pronounced. Overall, growth momentum remains subdued. Against this backdrop, the US Federal Reserve (Fed) faces an extremely challenging task, as the inflation rate is also above 4 percent.

Growth, sentiment and trend

In percent

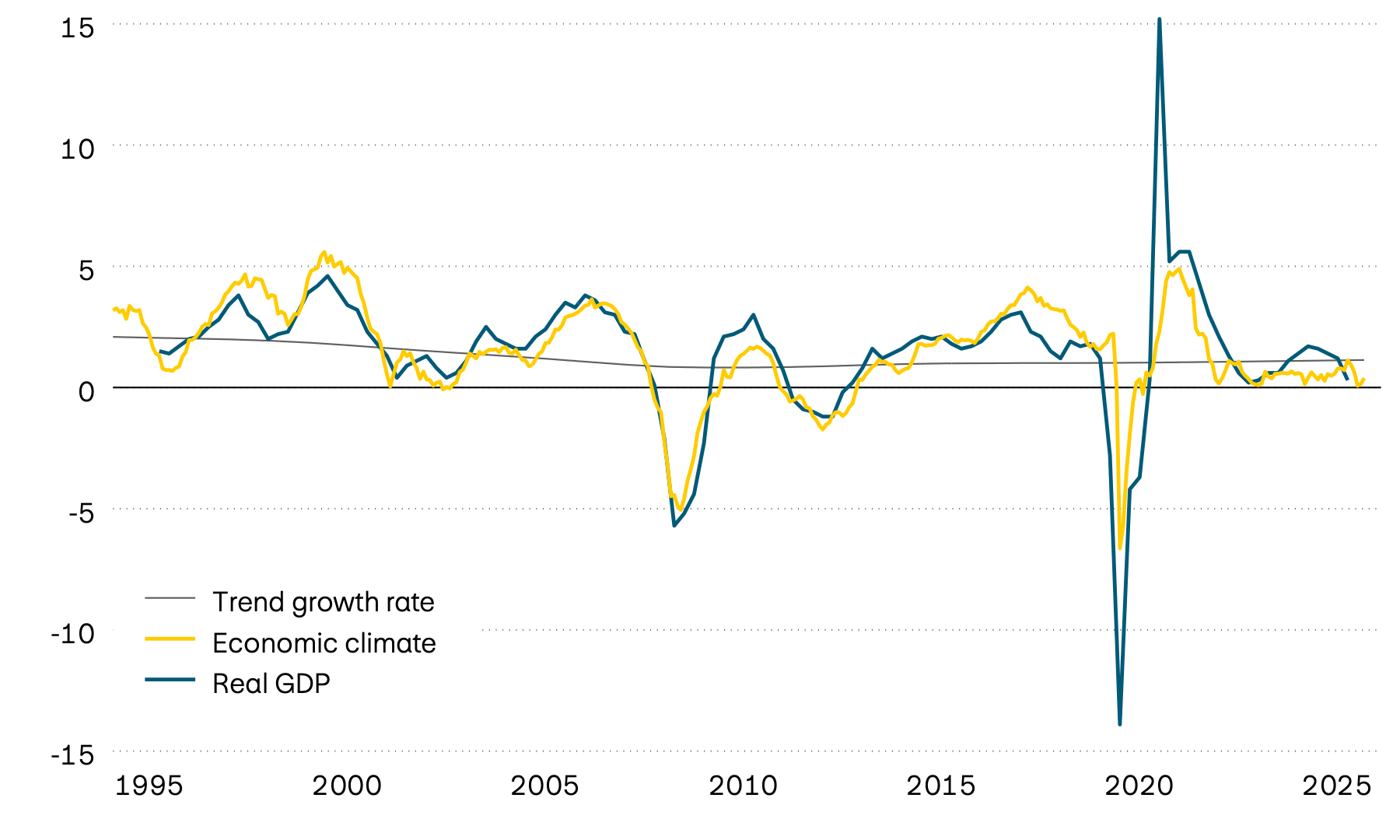

Economic activity in the eurozone remains subdued for the time being. There has been a certain weakness in demand in the services sector in particular, which reflects continued restraint and pessimistic sentiment among consumers. Stagnant foreign trade is also holding back economic development. However, industrial companies have become somewhat more optimistic again recently, reporting rising order intake. Inflation also stabilized recently: the overall rate fell from 3.2 percent in May to 2.8 percent in June. This is primarily due to the lower oil price, but prices in the services sector are also no longer rising as sharply in light of the weak economy. This has eased the pressure on the European Central Bank (ECB) to take further action after it raised its key policy rate by 0.25 percentage points in June.

Growth, sentiment and trend

In percent

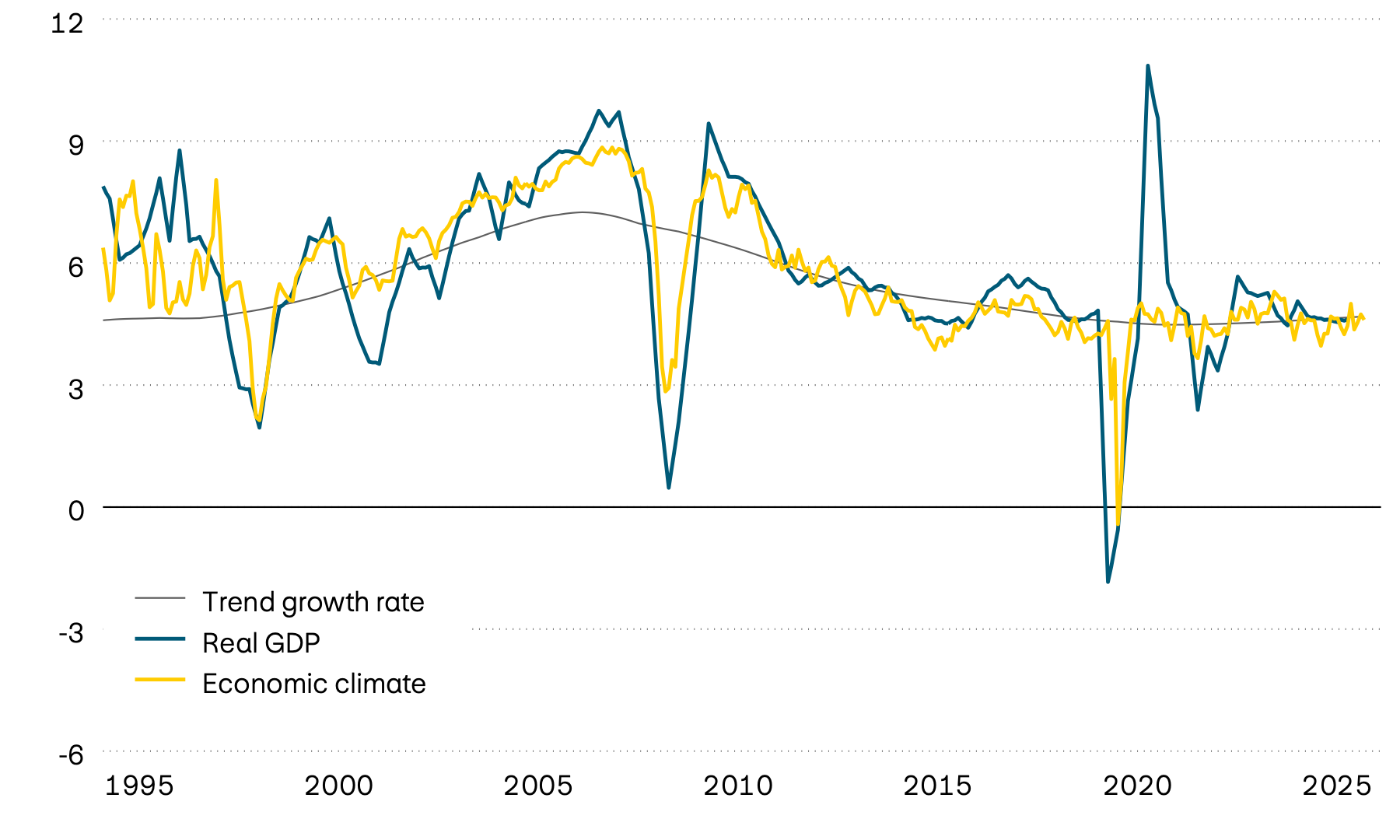

Asia’s major emerging markets are particularly exposed to the ongoing conflict in Iran due to the high trading volume with the Gulf region. The associated restrictions in the Strait of Hormuz have not yet been sustainably resolved, despite repeated efforts to achieve a ceasefire and negotiations on a peace agreement. That said, economic activity remains solid in many economies, partly because countries such as South Korea and Taiwan are benefiting greatly from the strong demand for computer chips, thanks to their important role in the value chain. China continues to paint a different picture: the world’s second largest economy is still struggling with serious economic problems. Investments are now well below the previous year’s level, and consumer spending is also down on last year.

Growth, sentiment and trend

In percent

Global economic data

| Indicators | Switzerland | USA | Eurozone | UK | Japan | India | Brazil | China |

|---|---|---|---|---|---|---|---|---|

| Indicators GDP Y/Y 2026Q1 |

Switzerland 0.5% |

USA 2.7% |

Eurozone 0.3% |

UK 0.9% |

Japan 0.4% |

India 7.8% |

Brazil 1.8% |

China 5.0% |

| Indicators GDP Y/Y 2025Q4 |

Switzerland 1.0% |

USA 2.0% |

Eurozone 1.2% |

UK 0.9% |

Japan 0.3% |

India 8.0% |

Brazil 1.8% |

China 4.5% |

| Indicators Economic climate |

Switzerland + |

USA – |

Eurozone = |

UK = |

Japan + |

India – |

Brazil – |

China = |

| Indicators Trend growth |

Switzerland 1.2% |

USA 1.7% |

Eurozone 0.8% |

UK 1.8% |

Japan 1.1% |

India 5.3% |

Brazil 2.1% |

China 3.6% |

| Indicators Inflation |

Switzerland 0.5% |

USA 3.5% |

Eurozone 2.8% |

UK 2.8% |

Japan 1.5% |

India 4.4% |

Brazil 4.7% |

China 1.0% |

| Indicators Policy rates |

Switzerland 0.0% |

USA 3.75% |

Eurozone 2.4% |

UK 3.75% |

Japan 1.00% |

India 5.25% |

Brazil 14.25% |

China 3.0% |

Source: Bloomberg